The annual Open Enrollment Period began on November 1, 2025, amid uncertainty surrounding the possible extension of tax credits that make healthcare coverage affordable for millions of people. Below, we address some of the most frequently asked questions about this year’s health enrollment period.

It is an annual window during which individuals in the United States can purchase a health insurance plan or make changes to their current plan.

From November 1, 2025, to January 15, 2026.

However, states that run their own marketplaces may already have allowed people to start making changes to their healthcare coverage and/or may close the enrollment window at a later date.

Depending on where you live, your state may allow you to purchase a healthcare plan through the federal marketplace, or may run their own marketplace and website.

States with their own marketplace and own platform: California, Colorado, Connecticut, Georgia, Idaho, Illinois*, Kentucky, Maine, Maryland, Massachusetts, Minnesota, Nevada, New Jersey, New Mexico, New York, Pennsylvania, Rhode Island, Vermont, Virginia, Washington, and Washington D.C. *Illinois switched to a state-run marketplace for this year’s Open Enrollment Period.

You can access the federal and state marketplaces here.

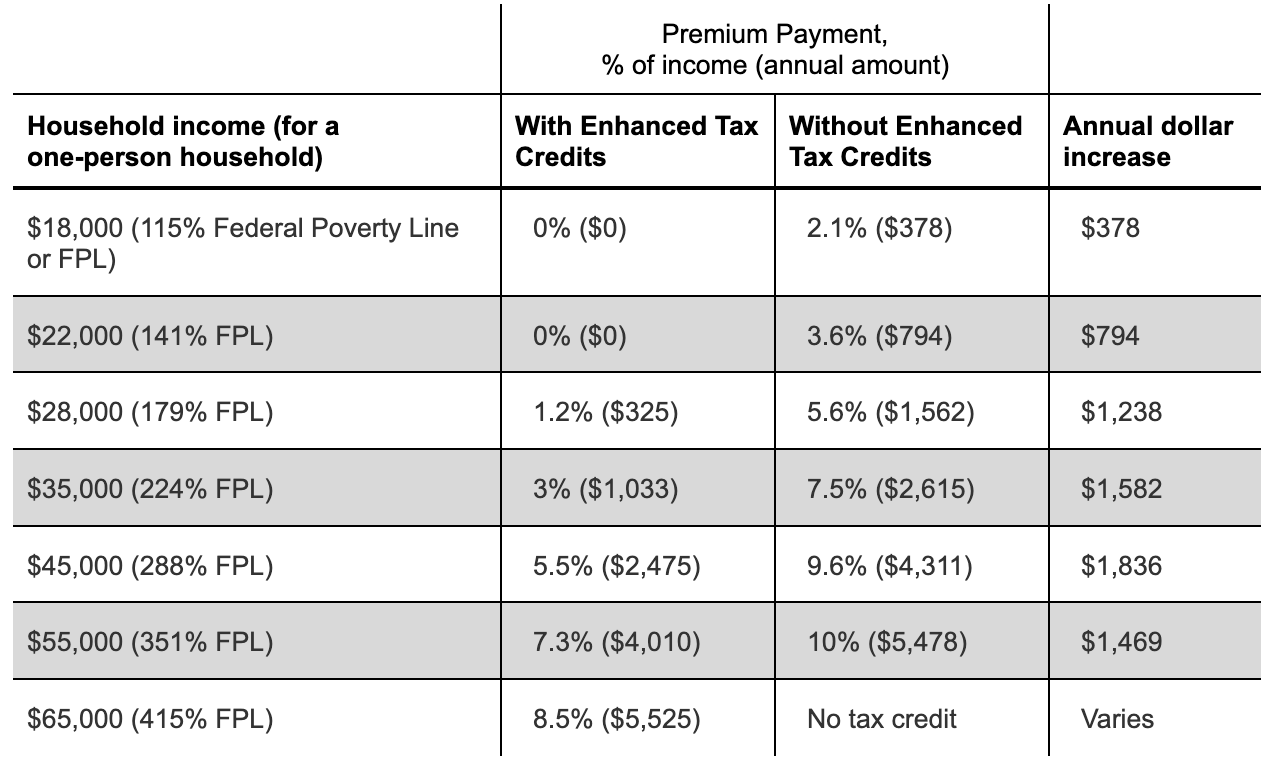

At the center of the federal government shutdown is members of Congress’ inability to come to an agreement on extending the Enhanced Premium Tax Credits that alleviate the cost of healthcare for many. These subsidies were first introduced in 2021 and extended through 2025 by the Inflation Reduction Act (IRA). The tax credits are a form of subsidy that helps people access healthcare by lowering the share of the monthly insurance premium they pay. Since their introduction, they have doubled the number of people covered by marketplace health insurance plans. Without extending these tax credits or setting up another subsidy, millions of people could face higher coverage costs or lose coverage altogether.

According to the Kaiser Family Foundation, with the tax credits, a person making $28,000 a year would have to pay no more than 1.2% of their annual income, or $325, towards a basic healthcare plan. Without them, that same person would pay no more than 5.6% of their annual income, or $1,562, towards that same plan. In other words, this person would see an increase of more than $1,000 in their out-of-pocket costs from one year to the next. The following table illustrates the differences in out-of-pocket costs for individuals at different income levels.

In accordance with longstanding federal policy, undocumented immigrants are excluded from purchasing healthcare coverage through the marketplace or having access to care through federal programs like Medicaid and Medicare. DACA recipients were previously eligible to purchase marketplace plans last year. They were stripped of that eligibility under a rule finalized by the Centers for Medicare and Medicaid Services (CMS) in June 2025.

Both groups may still purchase a private, unsubsidized health insurance plan directly through insurance providers, although this is financially inaccessible for many.

Other groups of migrants may continue to purchase plans on the marketplace, but will no longer be eligible for subsidies to lower their monthly premiums, effective January 1, 2027. This includes:

Legal Permanent Residents (LPRs), certain Cuban and Haitian migrants, and Compact of Free Association migrants (Micronesia, Marshall Islands, and Palau) migrants continue to be eligible for marketplace plans, subsidies, and federal healthcare programs.